A CEO of a multi-billion-dollar company to CFO: “Why are the numbers constantly changing? Doesn’t the team know what’s going on? Are they incompetent?”

Well, maybe. That’s one possibility. But let’s explore also some of the other options.

One often overlooked reason is that the question is wrong. If you’re modeling a probabilistic real world with deterministic numbers, you’d expect them to change.

In fact, it’s when they stay the same that you should be worried. When that happens, it’s either no one is paying attention, deliberately hiding the truth or making some really stupid decisions just to ‘hit the plan.’

Either way, it’s not good.

The thinking that ‘hitting the static plan’ is a sign of ‘good execution’ and competence is often driven by some form of: “Winners don’t make excuses; they simply deliver the results.”

While that is indeed a great rule to live by when the targets are not ‘stupid,’ constantly ‘hitting’ a static plan doesn’t qualify. It’s not a sign of competence. The odds are it’s more likely a sign of lying and cheating.

Great performance is not a static line that you hit all the time. The only way you hit a static plan consistently is by lying about how challenging the plan is in the first place or using artificial gimmicks to distort the results to fit the plan.

So, there’s that. That’s one reason. The expectations may be ‘stupid.’

That, however, doesn’t mean accepting poor performance (which is often the straw man conclusion from above). Let’s come back to that later.

First, let’s list some other reasons why the numbers are constantly changing.

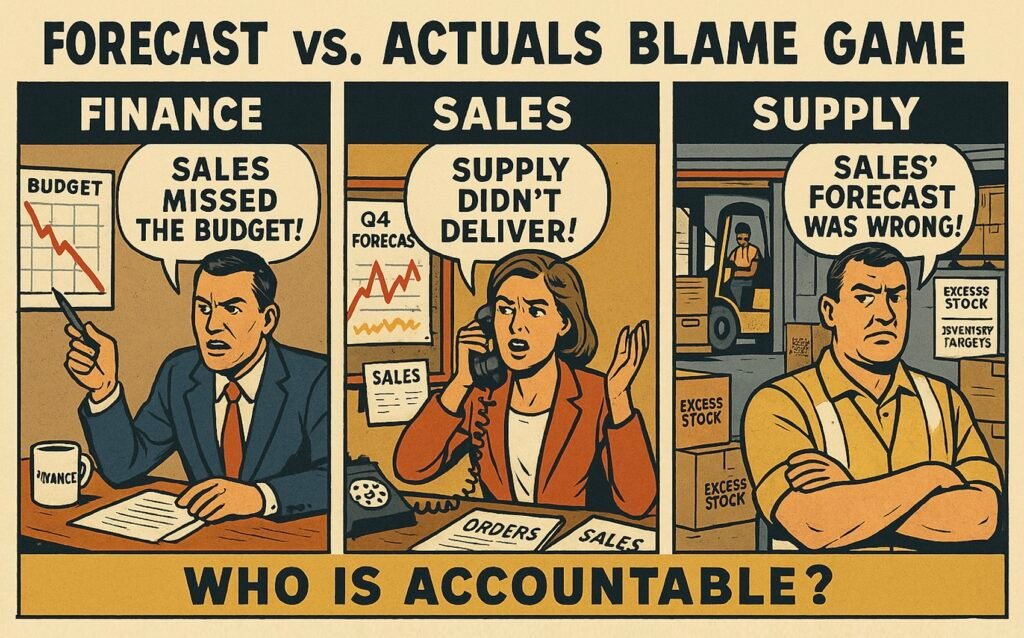

Lack of effort is definitely one. Ever heard a version of this: “Sarah didn’t have a chance to look at the numbers earlier. Now, when she did, she discovered a few things that were wrong or missing.” Or this, “Well, we closed (or other times, lost) couple new customers, but finance wasn’t aware of them.”

In other words, not all relevant stakeholders care a lot about what’s in (or missing from) the numbers. We’ll get back to why this is and what can be done about it later.

Lack of skills is another one, often corollary to the previous point. For example, the plan is based on John’s complicated and detailed Excel file in the FP&A department, and since it models ‘everything’ at the level of atoms, the numbers change if someone as much as sneezes in the vicinity.

In other words, planning out of the joy of planning, but little to do with performance.

Here’s one that is a difficult pill for senior executives to swallow: they don’t listen. Or they may ‘listen,’ but by their actions, they make it against anybody’s interest to tell the truth. And as a result—what a surprise—they don’t hear the truth, until it inevitably comes through in the actuals.

This goes both ways. People don’t tell negative things because they get reprimanded and micromanaged as a consequence. They are not transparent about positive opportunities because those quickly become new promises they are held accountable for delivering.

The organization may know well, or at least much better than what is reflected in their numbers, what is really going on. But if the executive mindset is that the figures ‘must align with the annual budget,’ (or some other silly nonsense like that) that’s what they are going to hear—regardless of whether it aligns with reality or not.

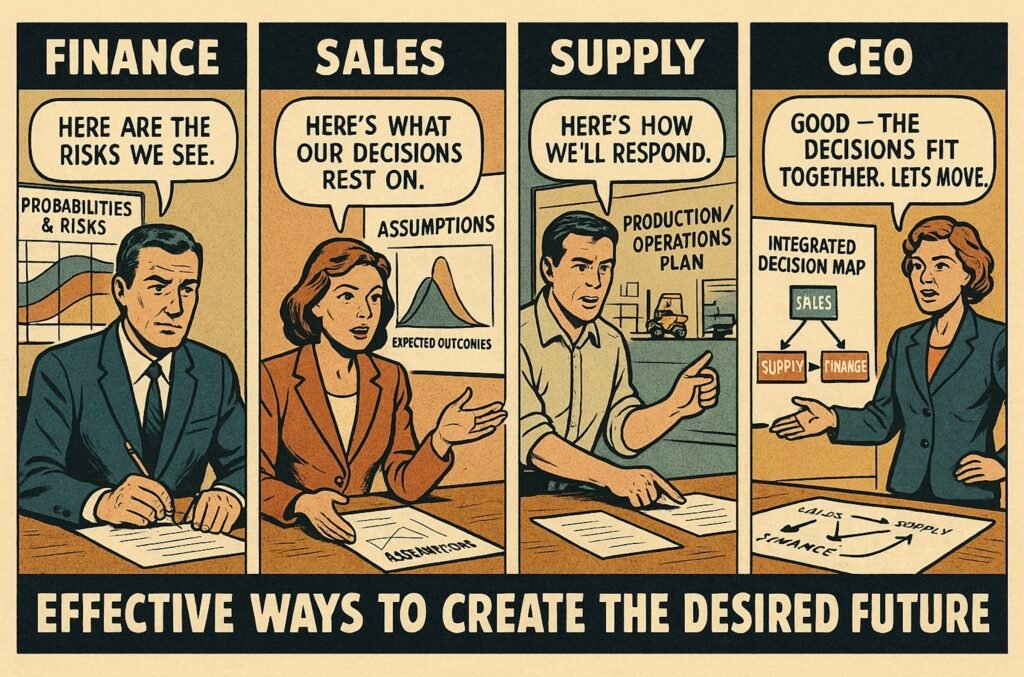

Here is one that many do: accountability for the numbers (rolling plans) is not where the business accountability is. For example, a separate planning team is creating a sales forecast, while sales has no real accountability for what goes into it or what happens as a consequence. Or, at the very least, the have much higher conflicting accountabilities, like ‘hit the static plan for this year.’

Common arguments for this are ‘to save time,’ ‘not to worry about the decimals,’ ‘to be more accurate,’ or the ‘business needs to focus on business.’

However, while a planning team somewhere else may be able to create a roughly correct (or even significantly better) forecast faster than if that accountability were, for example, with sales, it also disconnects the accountability of planning from ‘natural’ business accountabilities, and plans from real decisions and assumptions.

And no, that doesn’t mean that sales directors should do forecasting. That’s a waste of their time. They don’t have the right skills nor the time.

As a corollary to that, many companies, for some reason, want to implement planning processes that misalign with incentives. For example, running ‘rolling forecasting’ that looks 18 months forward, while sales is incentivized to ‘hit the plan’ for the calendar year, at all costs.

While there may be some half useful use cases where that doesn’t matter, don’t be surprised if the plans change without solid connection to reality: after all people dealing with the reality, don’t have ‘any skin in the game,’ what goes on in the planning processes.

Finally, a bit ironically, one of the reasons the numbers keep changing is because executives are focused on the numbers. Numbers represent outcomes, that cannot be controlled. That doesn’t mean that they are not important, rather by focusing on them you can end up neglecting real-life factors (assumptions) behind the numbers.

So, there you have it. So far, we’ve listed about half a dozen possible reasons why the numbers keep changing. How do you know what’s the issue and what to do about it?

As with everything, a good place to start is to make sure your requirements are not ‘stupid.’ If you’re expecting that a set of static deterministic numbers will describe reality unchanged over time, well then, as the MythBusters would say: “There’s your problem.”

Ironically, demanding static numbers to remain the same (it’s impossible) likely contributes to the fact that the ‘truth’ is revealed bit by bit—even though most of it is known earlier. And if your behavior is to punish anyone who tells the truth, you will never hear the truth. It really is that simple.

What to do about it? Always praise people for telling the truth. How to do that, and how does that not lead to accepting poor performance? The answer to both is that your focus needs to be on the assumptions (real-world factors) rather than the numbers. Even better, use probabilities to describe the future.

Assumptions will reveal if you have a performance issue, or if the reality has changed. What was the original business logic, and how has that changed?

Sales of 90 when the target was 100 is poor performance if the target was based on the market growing 10%, but not if it stayed flat (simplified to make the point).

Note, also conversely, sales of 100 is poor performance if the actual market grows 20%, instead of 10% as assumed in the target.

The point is not to get caught on individual facts, rather it’s that the level of performance depends on the real-world context as a whole.

However, they work also only up to a point. It’s impossible to describe all possible real-life factors, or to predict their impacts precisely. But using probabilities can fix that. Instead of saying the sales will be 100, say there is 80% or 90% likelihood that the sales will be 100 or more (simplified to make the point).

Even if you’re never able to predict the future precisely, your predictions can be accurate, or at least more accurate, when using probabilities.

Rigorously debate, test and revise the assumptions and the probabilities. That strengthens the business logic behind the numbers, which, as a consequence, will make the numbers more robust.

Then the volatility that is left is mostly reflecting the volatility of the real-world. There is nothing you can do about that, nor should you. The job is to improve performance under that uncertainty, not naively attempt to make the real-world static.

Regardless of the uncertainty, you can always improve the odds that decisions will win, and the expected values over the long-term will be better.

Similarly, praise that the change in assumptions is taken into account in the new plan, but hold the organization accountable for finding new opportunities that are realistic but challenging under those conditions (instead of conditions from 12 or some arbitrary number of months ago that are disconnected from reality).

For this to be effective, target-setting should (probably) be probabilistic and dynamic, and cover the planning horizon.

In other words, targets should remain realistic and challenging under various future scenarios, and in order to avoid rewarding ‘dumb luck’ or punishing for ‘noble failures’ account for the influence of luck.

And if the targets for some reason become obsolete, change them.

Amazon avoids many of such pitfalls by focusing on input metrics instead of output metrics. For a simple reason: the organization cannot control outputs, but if they have the right focus on the inputs, the outputs will follow over time.

Another simple but crude method of incentivizing truth-telling is to use bias of the plan as a bonus measure. A common counterargument is that this distorts efforts from ‘real business,’ such as selling more.

And while that may be true in some individual cases, it overlooks the fact that the bigger that problem is, the bigger the bias in the number. And that, in turn, means the big picture is distorted over a long period, and the negative effects of that are always far greater.

Bias measures, by definition, allow inaccuracies (being over or under the estimations) over short periods of time and impact behavior only when there is a systematic error (significant continuous distortion of reality) over the long term.

Aligning targets is also key to aligning incentives. As long as sales are incentivized to hit a static number for the year, do not wonder if the truth for that year is revealed ‘bit by bit’ or if no one cares what goes into the rolling plan for the next year.

Similarly, planning accountabilities must align with business accountabilities. If the plan is updated by finance, no matter how ‘good’ it may be, from sales’ point of view, it’s finance’s plan, not their plan.

The professionals doing the sales forecast should report to the people accountable for the business results. Not because of speed, accuracy or lack of, but to establish clear ownership for what goes into the plans and what happens as a consequence.

Otherwise, there will always be a million things that ‘turn out to be relevant’ (will be used as an excuse) and are either not included, misunderstood, or added unnecessarily.

Lack of accountability or incentives is the reason why people ‘don’t care,’ i.e., why they ‘are not onboard’ with the fancy new planning process. Don’t ask why sales isn’t interested in what’s in the FP&A team’s Excel file for next year if they are accountable for delivering a fixed number for this year.

If you fix incentives and accountabilities and restructure reporting lines accordingly, any remaining skill issues are almost automatically corrected. Not over night, but eventually.

As soon as there are clear incentives and accountabilities, supported with top management behaviors to tell the truth and drive performance, people will find resolutions to any gaps in planning skills.

So, there you have it: that’s why number are changing.

After you have checked all these boxes—aligned incentives, accountabilities, and reporting lines; made your requirements ‘less stupid’; incentivized truth-telling; focused on assumptions instead of the numbers; and used probabilities to describe probabilistic reality—if the numbers are still changing, then it’s likely a competence issue.

However, without addressing these issues first, you can’t really tell, and treating the numbers changing as a competence issue, won’t necessarily deal with real root causes.

Practical insights

- Expectations that reality aligns with static deterministic plans are stupid.

- Use probabilities to describe reality, which is probabilistic.

- Align planning accountabilities with business accountabilities.

- Align incentives with expected behaviors.

- Incentivize truth telling over ‘hitting’ a static plan disconnected from reality.